beEdison is a Finalist in the 2015 “Finance for Resilience” competition!

Finance for Resilience (FiRe) is an open and action-oriented competition platform that collects, develops and helps implement powerful ideas to accelerate finance for clean energy, climate, sustainability and green growth. FiRe, which is run by Bloomberg New Energy Finance, focuses on interventions that are led primarily by the private sector, bear the potential of significant incremental finance and can be implemented independently from the international policy process of climate change.

This year beEdison, with the support of truSolar’s working group members, submitted an intervention titled: “Automating a Fico-like risk score for clean energy.” The submission was judged by a panel of renewable energy experts along with 51 other entries, and was selected as one of eight finalists to present at this year’s “Bloomberg Future of Energy Summit.” beEdison’s intervention is grounded in big-picture thinking, and has at its core a sharply delineated focus: we must lower transactional soft costs for commercial clean energy projects and promote clean energy asset securitization by scoring risks in a standardized way.

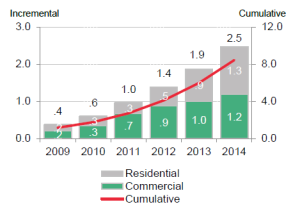

The Challenge: The starting point for beEdison’s invention lies in the recognition of a key challenge facing market participants who want to expand clean energy deployment. Currently, the commercial & industrial sectors consume 51% of America’s energy, twice as much as residential and more than residential and transportation combined. Yet, in 2014, after several years of shared leadership, C&I was overtaken by residential in total solar capacity installations. Why this happened reveals how the C&I segment can and should adopt ready solutions to unleash growth, such as: 1) a reliable framework for credit assessment like FICO, and 2) standardized contracts, transaction practices, and cloud technology for solar asset buyers and sellers that enable growth to match and exceed residential proportionate to its actual share of electricity consumption.

The Solution: A widely-adopted, cloud-based software platform (beEdison) is needed to streamline/standardize commercial diligence, while providing reliable and uniform scoring metrics for financiers to use. Such a platform using industry accepted diligence and rating standards (truSolar®) will lower project costs, improve deal conversion ratios and accelerate solar asset securitization.

Scope: beEdison and truSolar will initially promote greater funding inflows into the USA’s non-residential solar market, before platform expansion occurs in markets such as Europe, Australia/NZ, Latin America and Africa. The beEdison executive team will also collaborate with industry leaders in other renewable energy sectors to devise project due diligence standards that are suitable for adjacent markets such as energy storage, energy efficiency, biomass, and other complex asset classes such like infrastructure-as-a-service.

Scale: By 2018, wide adoption of beEdison software solutions can unlock hundreds of millions of dollars in additional annual investment in US non-residential solar. Higher conversion ratios and soft cost reductions contribute to this additional capital deployment. There will also be secondary benefits that impact our environment and the capital markets. An additional 1.6GW of solar installed by 2018 would reduce carbon emissions by approximately 1.6 million metric tons: the equivalent of removing 351,000 cars from our roads. In addition, the widespread adoption and acceptance of beEdison project scores will facilitate securitization of solar project assets in the financial markets: this development will provide investment managers with additional capital deployment options.

The beEdison team knows there is a lot of work ahead. As a company we are committed to breaking down the market’s resistance to change by building trust between partners; securing acceptance of the truSolar Risk Screen Methodology by industry participants, notably financiers, rating agencies and solar project developers; and investing in efforts to convene industry players who can formulate and publish complementary risk screen methodologies for wind, biomass, biofuels and geothermal investment opportunities.

Join us on this mission! Contact join@beEdison.com for more information about beEdison’s software and project rating solutions.